Arbitraging Options Against Prediction Markets Is Harder Than You Think

Old-school betas, cross-asset hedges, and where things get messy fast.

The journey of almost everyone who looks into arbitraging options against prediction markets tends to follow the same path:

A prediction market implies a 20% probability that SPY closes above $X today, offering roughly a 5x payout if it happens.

At the same time, the equivalent X-1/X SPY call spread is trading for around $0.20, also offering roughly a 5x payout if SPY closes above $X by expiration.

So naturally, the first reaction is:

“Oh well, the market is efficient and that’s all there is to it.”

Now, it isn’t a totally wrong premise, but it is a bit… lazy.

After all, options and derivatives are not just things to bet on, but rather instruments that can be decomposed on an atomic basis to replicate any view, payoff or hedge you want.

So, there must be some way of combining the two in a +EV fashion, right?

As you’ll see shortly, the answer to that is a little muddy.

So today, we’re going to be taking a look at the nuances and edge cases that come up when you try mashing these derivatives together in a genuinely profitable way.

We’ll see where the market is efficient, where it isn’t, and walk through a few pathways most prediction market traders haven’t considered yet.

Without further ado, let’s get right into it.

What the Options Chain Already Knows

Before going any deeper, it’s important to understand how options are combined to generate implied probabilities.

The simple version is as follows:

Implied Prob ≈ Spread Value / Spread Width

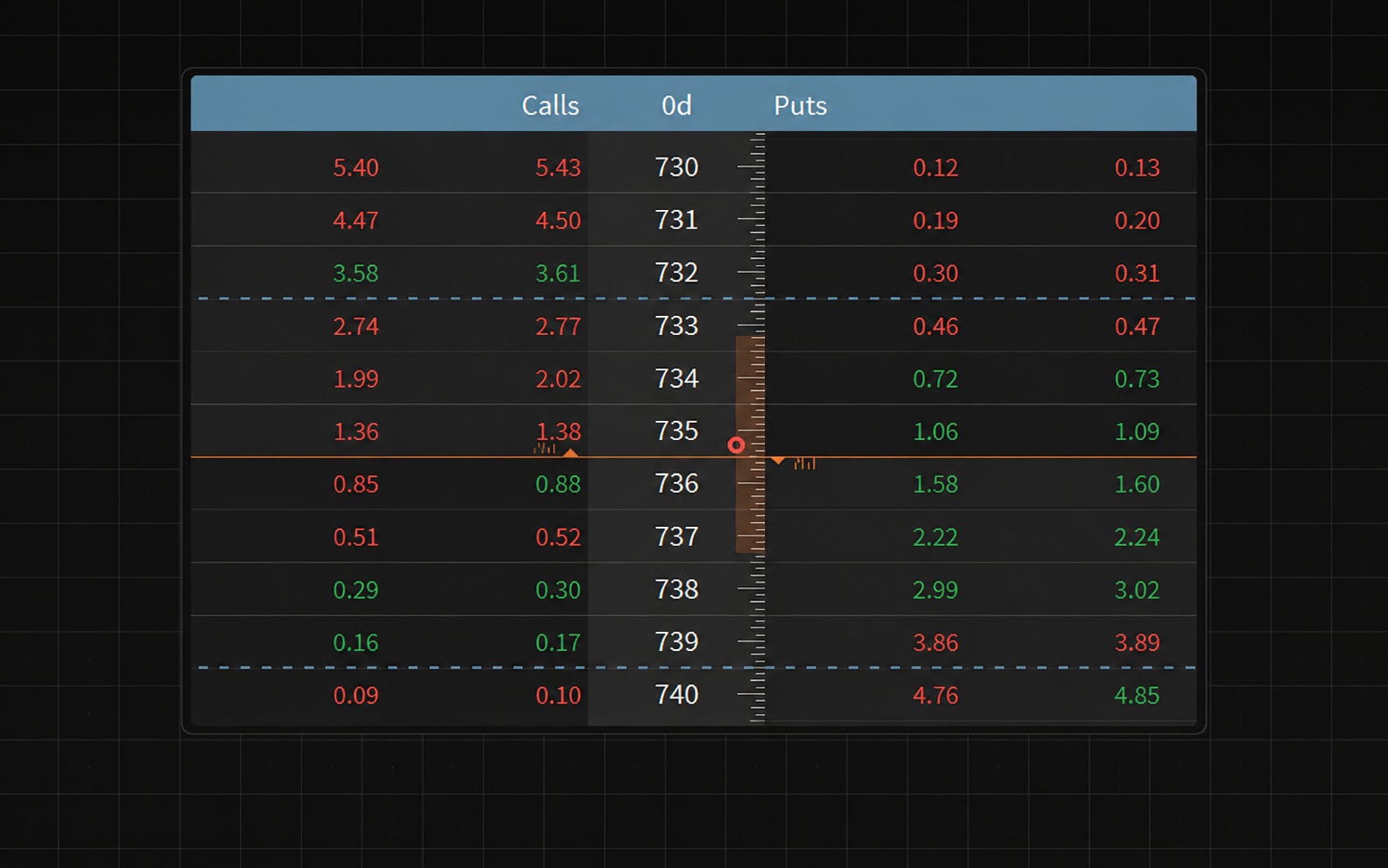

Assume you buy a 739 strike call and simultaneously sell a 740 strike call, for a total cost of $0.20.

The distance between strikes (the width) is $1.

The spread costs $0.20 to put on.

$0.20 / $1.00 → 20%

This is less rigorous than other methods like risk-neutral butterflies, but 9 times out of 10 it’s a solid approximation as it’s quite literally the payout odds the market is giving you for that view.

With that covered, let’s bring things back to prediction markets:

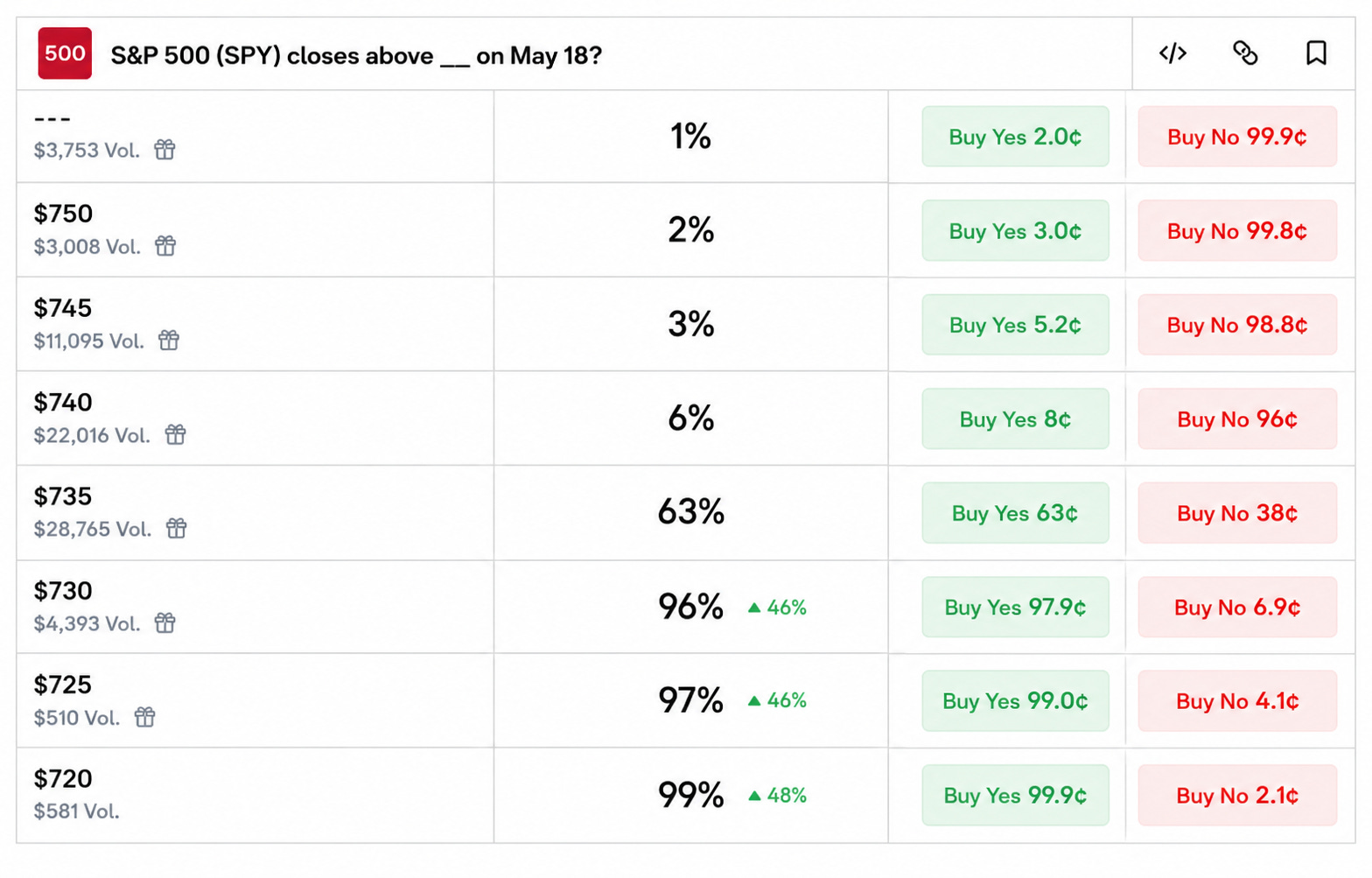

Pictured here is a market for whether the SPY ETF will close above a given strike price, K, on date t.

Say we had a view that on that date, the price would indeed be above $735.

The prediction market implies a 63% chance it’s true, paying out about 37%.

Now let’s see what the options market was offering at the same time:

The equivalent options position is a 734/735 debit spread, which pays out the max if SPY closes above $735.

Assuming midpoint pricing for simplicity, this spread would cost about $0.635, offering a payout of ~37%.

This 1:1 pricing is natural as low-latency infrastructure for stock quotes has become so commoditized that almost anyone can keep these two markets in line.

But as mentioned earlier, this is only the jumping-off point.